This August marks 20 years that Vladimir Putin is in power. The first decade his economic policy produced an unprecedented growth, but after Putin halted reforms the growthrate rapidly declined. Sergey Guriyev, chief economist at the European Bank for Reconstruction and Development, doesn't believe in recovery unless Putin radically reduces the state's role and protects property rights.

by Sergey Guriyev

In terms of economic policy, those 20 years fall into four distinct periods: the 'reform' years of his first term (1999-2003); the 'statist' years of his second term (2004 – the first half of 2008); the world economic crisis and recovery (the second half of 2008 – 2013); and the war in Ukraine, Russia’s growing isolation from the global economy, and stagnation (2014 – present).

The so-called 'Gref Program' was approved by the government in 2000 during Putin’s first term.

Interview with the Financial Times, 27 June 2019. Photo Kremlin.ru

Interview with the Financial Times, 27 June 2019. Photo Kremlin.ru

Named after former Economic Development and Trade Minister Herman Gref and formally called the 'Program for the Socio-Economic Development of the Russian Federation for the Period 2000-2010,' it introduced tax and progressive pension reforms, saw the adoption of the Land Code, greatly reduced barriers to opening and conducting a business, launched civil service reforms, and stepped up negotiations on Russia’s accession to the WTO. This led to a sharp acceleration of economic growth, an influx of foreign investment and the strengthening of the ruble.

The second term differed significantly from the first: according to the Gref program’s authors, reforms were only 30% complete when the process was halted.

Unprecedented growth

What’s more, the nationalization of the economy began. Significant reforms continued only in the macro-economic and financial spheres. The state debt was almost completely paid off and the Stabilization Fund was created.

The deposit insurance system was introduced, providing a key element in the competitive banking system that gave depositors confidence in not only Sberbank and other state banks, but also in their private competitors. Lower inflation and the introduction of deposit insurance created new opportunities for the development of the financial sector and the growth of corporate and retail lending. Macroeconomic stability and the assignment of investment ratings led to a major increase in foreign investment.

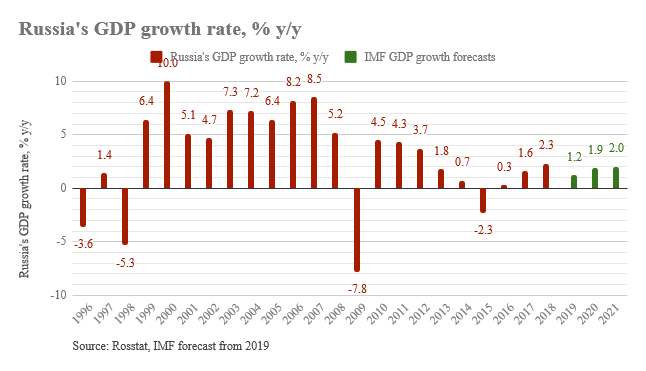

The reforms definitely produced tangible results. Gross domestic product grew at an average rate of 7% during Putin’s first term and during that part of his second term in which the reforms of the first continued to bear fruit.

Picture BNE IntelliNews

Picture BNE IntelliNews

In the 10 years from 1999 to 2008, Russian GDP grew by 94% and per capita GDP doubled. This is the most outstanding decade in Russian economic history — with the exception of the economic recovery after the Civil War with the help of the New Economic Policy (NEP). Even during Stalin’s industrialization drive, GDP growth per capita averaged only 5% per year.

Growth model exhausted

Because rising oil prices and the influx of foreign investment led to a significant strengthening of the ruble, GDP in dollar terms grew to 8.5 times its previous level — from $210 billion in 1999 to $1.8 trillion in 2008.

Of course, in addition to reforms, the fact that Russia had an underutilized labor force and unused production capacity contributed to the growth of Russian GDP, as did high global oil prices. According to various estimates, as much as one-third to one-half of the growth rate during Putin’s first decade in office is the result of the nearly eight-fold increase in oil prices, from $13 in 1998 to $97 per barrel in average annual terms.

It became obvious by 2008 that Russia had exhausted this model of growth. The production of shale gas was already growing and it was clear that shale oil would soon follow.

Russian enterprises were now complaining about a shortage of workers and only the country’s obsolete factories still stood idle.

What was needed was to accelerate reforms, not decelerate them. In 2008, the Russian government formulated and adopted its 'Concept for the Long-Term Socio-Economic Development of the Russian Federation until 2020.'

These reforms gave priority to Russia’s integration into the global economy, investment in human capital, and innovation. Speaking to the State Council in 2008, President Vladimir Putin said, 'If we continue on this road we will not make the necessary progress in raising living standards. Moreover, we will not be able to ensure our country’s security or its normal development. We would be placing its very existence under threat. I say this without any exaggeration.'

No reforms during global financial crisis

Russia, however, did not carry out any reforms during the global financial crisis.

And after the crisis it did not immediately resume discussions about why the pre-crisis growth model had lost effectiveness. In 2010, Oleg Tsyvinsky and I co-authored an article for Vedomosti, 'Scenario 70-80,' in which we warned that Russia was headed for stagnation and would lose what had been gained from a decade of growth.

We predicted that if oil prices rose as high as $70-$80 per barrel, Russia would return to the political and economic model of the 1970s-1980s. (That scenario is treated in more detail in the first chapter of the book 'Russia after the Global Economic Crisis,' published in the U.S. in 2010 and in Russia in 2011.) That is exactly what happened: the average annual growth rate during the 10 post-crisis years (2010-2019) has remained less than 2%.

The authorities continued to discuss and promise reform.

They gave up on plans for long-term development, but in January 2011, Putin instructed the Higher School of Economics and the Presidential Academy of National Economy and Public Administration to create a new Strategy 2020. This led to the creation of 21 working groups involving a wide range of experts who developed a full-scale reform program. The Strategy 2020 they authored called, above all, for the creation of a 'new model of economic growth.' It also recommended the removal of barriers to doing business and investment in human capital.

For his next presidential run in 2012, Putin had yet another development program drawn up. The economic part of that program was published in Vedomosti on January 30, 2012 under the heading: 'We Need a New Economy.' On May 7, 2012, Putin signed his 12 so-called 'May decrees,' including one that dealt with long-term state economic policy. It called for a radical improvement in the investment climate and a major scaling back of the state’s presence in the economy, predicting that this would lead to 1.5 times greater labor productivity over seven years (meaning 6% per year) and an increase in investment to 27% of GDP.

The promised reforms never materialized, so it is unsurprising that it proved impossible to achieve the economic results which had been hoped for.

Rapid decline

After a short-lived post-crisis recovery in 2010-2011, the growth rate began a rapid decline, falling to just 1.8% of GDP in 2013.

The subsequent decline in oil prices, war, and isolation from the global economy buried any hopes of reform and of accelerating economic growth. In place of 6% average annual GDP growth in 2012-2018, the rate never exceeded 1%. In dollar terms, Russian GDP remained at 2008 levels and now equals not 3% of global GDP as it did as recently as 10 years ago, but just 2%. Investment did not grow to 27% of GDP, but remain at 20%-22%. Foreign investment has fallen substantially and capital flight has accelerated. In 2014-2018 alone, those losses totaled $320 billion, or approximately 4% of GDP per year.

The Russian authorities, of course, noted the disappointing economic results of recent years and investors’ lack of faith in the prospects for reform and again began thinking about a 'new model of growth.'

Little trust in public investments

Instead of one more iteration of liberal programs, the new 'May decrees' that Putin signed in 2018 rely on public rather than private or foreign investment. The so-called 'national projects' it envisions will cost Russian taxpayers and pensioners many trillions of rubles. The idea is that this approach will help the Russian economy grow faster than the world rate of growth.

The problem is that neither the markets nor the experts have faith in it. Russian assets continue to be traded at a significant discount, and the IMF predicts that Russian GDP will grow by an annual average of just 1.4% through 2023. By this reckoning, Russian GDP in 2023 would equal $1.8 trillion — exactly where it stood in 2008 — with the result that Russia’s share of the global economy would total just 1.7%.

It is not surprising that experts and investors have little faith in the effectiveness of large-scale public investment in a country notorious for corruption. The solution to Russia’s problems lies in precisely the opposite direction — in implementing the long-promised reforms: protecting property rights, respecting the rule of law and competition, reducing the state’s role in the economy, fighting corruption, reintegrating Russia into the world economy, and investing in human capital.

Sergey Guriyev wrote this article for Vedomosti. The Moscow Times allowed us to republish the English translation.

For more economic and social data see BNE Intellinews Putin's 20 years on the job in numbers