President Trump's current sanctions policy provides a critical economic lifeline to Moscow. At the same time, the U.S. is shifting an unsustainable fiscal burden onto Ukraine. By delaying secondary sanctions, Russia is able to absorb wartime costs, writes economist Oleksandra Moskalenko. Meanwhile, Ukraine’s own economic stability is eroding ever further. A decisive shift toward comprehensive enforcement of secondary sanctions is not merely an option, but a strategic imperative to accelerate the conflict's resolution.

President Zelensky in the White House with President Trump, August 2025. Photo: Andrew Caballero-Reynolds / ANP / AFP

President Zelensky in the White House with President Trump, August 2025. Photo: Andrew Caballero-Reynolds / ANP / AFP

On September 13th, Donald Trump issued yet another conditional threat against Moscow. Writing on his Truth Social platform, he declared that the United States would impose ‘major sanctions on Russia’ only if all NATO members agreed to follow suit, halted oil purchases, and simultaneously imposed tariffs of up to 100 percent on China.

This marks the latest ultimatum to dissolve into strategic inaction. In July, Mr Trump had pledged to enforce sweeping secondary sanctions on Russia’s oil trade partners by August 8th if Vladimir Putin did not halt his aggression. The deadline passed without consequence.

Now the conditions have been raised so high that they appear designed never to be met. For the Kremlin, the pause is a gift: time to adapt, time to collect revenues, and time to reposition itself diplomatically. Russia is not just ‘getting a reprieve’; it is actively weaponizing time against the West's electoral cycles and Ukraine's finite resources.

A decisive Ukrainian victory requires a three-pronged assault on Russian capabilities: battlefield dominance, fiscal strangulation via comprehensive secondary sanctions, and sustained budgetary support for Kyiv. The current U.S. policy actively undermines two of these three pillars, creating a strategic vulnerability that prolongs the conflict.

Breathing space for Moscow

Secondary sanctions are designed to punish not only Russia itself but also the foreign banks, insurers, and shippers that keep its oil and gas exports flowing. Applied comprehensively, they would render Russian crude effectively toxic, raising risks and costs for buyers and draining revenues from the Kremlin’s federal budget.

Mr Trump’s new conditions defer this outcome. By tying U.S. enforcement to NATO unanimity, he has handed countries such as Hungary and Turkey an effective veto. Both continue to buy Russian oil and show little sign of shifting course. As a result, Moscow retains access to its most vital lifeline: energy revenues.

This reprieve comes just as Russia’s economy is showing strain. According to Bloomberg and Agence France-Presse, the cracks are widening:

- The Central Bank has cut its key interest rate from 18 percent to 17 percent to counter stagnation, the third reduction since the rate was pushed to 21 percent in September 2024.

- Car sales fell by 30 percent in June.

- Domestic steel demand is forecast to shrink by 10 percent in 2025.

- Coal and metallurgy are hampered by shortages of Western machinery, with Chinese substitutes proving poor in quality and years late.

Major banks are quietly preparing for state bailouts as bad loans mount.

Enforcing secondary sanctions now would exploit these fractures and accelerate Russia’s fiscal exhaustion. Instead, current policy gifts the Kremlin critical room to maneuver. The pause allows it to reroute trade, expand its shadow fleet of oil tankers, and reassure partners such as China, India, and Turkey.

Ukraine’s mounting burden

While Russia benefits from hesitation, Ukraine faces mounting fiscal strain. According to the Ministry of Finance of Ukraine, in 2025 26.3 percent of GDP will be allocated to security and defense, with expenditures rising to about $40.9 billion (or about €34.5 billion). This represents only a modest 2 percent increase from 2024, but it underscores the growing cost of war for Ukraine. Every additional hryvnia spent on defense means less fiscal stability and fewer resources for hospitals, schools, and the well-being of people living under siege.

This increase in spending is intended to strengthen defense capabilities, yet the costs continue to rise sharply by the day. Roksolana Pidlasa, head of Ukraine’s parliamentary budget committee, estimates that daily war costs have risen from $140 million (€118 million) in 2024 to $172 million (€145 million) in 2025, in contrast to Russia’s daily war cost of $520 million. Looking ahead, former prime minister and current defence minister Denys Shmyhal has warned that Ukraine will require at least $120 billion (€101 billion) for defence in 2026 — a sum equal to nearly two-thirds of national GDP, which the IMF estimates at about $189 billion (or about €159 billion) in 2024.

The burden is unsustainable without external support. In 2024 the Ministry of Finance secured more than $41 billion (€34 billion) in external financing from eleven development partners. The United States provided $8.3 billion (€7 billion) in direct budget aid, roughly one-fifth of Ukraine’s external financing needs, while the European Union contributed $17.3 billion (€14.6 billion) in concessional loans and grants.

Ukraine’s financial burden is unsustainable without external support

In 2025, however, that U.S. budget support has been paused. No new grants to the central budget have been announced. Instead, President Trump has shifted toward a model in which NATO collectively purchases U.S.-made military equipment for Ukraine, while fiscal transfers stall.

According to the National Bank of Ukraine’s (NBU) July 2025 assessment, direct budget support through international financial assistance programs this year will amount to $53.7 billion (€45.5 billion), including loans, guarantees, and grants. Yet the United States has not resumed its direct budgetary assistance, and the prospect of renewal remains uncertain. The Kiel Institute for the World Economy reported that between March and April 2025, European donors allocated nearly €20 billion in combined military, humanitarian, and financial aid. This was the highest two-month total since the start of the war, and it partly offset the pause in U.S. support.

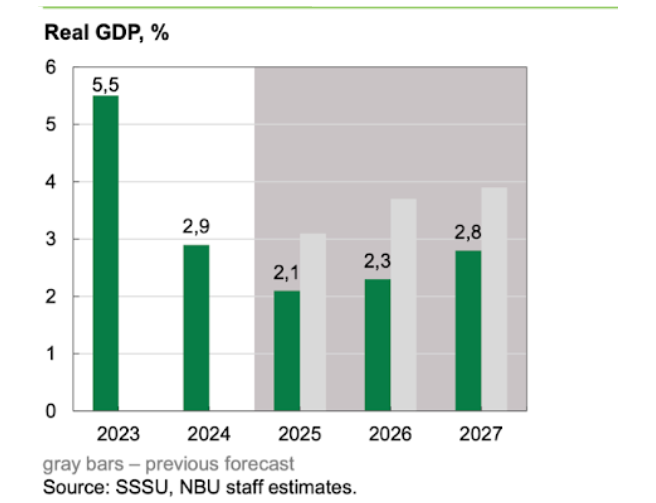

Meanwhile, Ukraine’s economy operates under extreme strain. The aforementioned NBU report highlights the broader economic picture. GDP growth is forecast at just 2.1 percent in 2025, down from 2.9 percent in 2024. Inflation, at 14.3 percent in May, is projected to ease to around 9.7 percent by year-end — still painfully high by pre-war standards. The fiscal outlook is even bleaker: the consolidated budget deficit is projected at 22 percent of GDP, requiring record external financing of $53.7 billion (€45.5 billion). Defense spending alone accounts for the overwhelming share of expenditure.

Source: National Bank of Ukraine. (2025, July 31). Inflation Report, July 2025 (Q3 2025).

This leaves Ukraine exposed. War cannot be fought with weapons alone. Soldiers and civilians alike depend on salaries, pensions, and social spending to sustain daily life. Without stable external budget support, Kyiv’s fiscal stability becomes fragile. Rising debt-service costs and a widening deficit risk destabilisation just as the war enters its fourth year.

Energy revenues and the burden of war for Russia

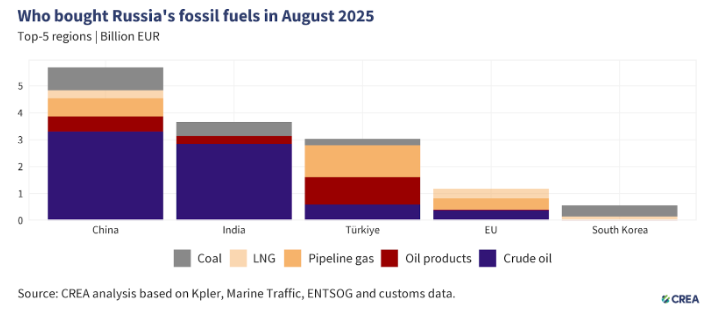

According to the Centre for Research on Energy and Clean Air (CREA), in August 2025 China remained the largest buyer of Russian fossil fuels, spending about €5.7 billion, followed by India with €3.6 billion. Turkey, a NATO member, ranked third with purchases worth €3.0 billion, mainly pipeline gas and oil products. The European Union as a whole spent about €1.2 billion, concentrated in Hungary and Slovakia, while France, the Netherlands, and Belgium recorded no significant imports. This demonstrates how NATO unanimity on sanctions is undermined by a few members that remain tied to Russian energy flows.

Moscow’s war economy has proven more resilient than many assumed, but that resilience should not be overstated. A Chatham House analysis by Timothy Ash notes that while Russia’s economy has shown itself to be more durable than many expected, this resilience comes at a cost: the country’s GDP is about 12 percent smaller than it might have been without war and sanctions, with cumulative losses exceeding $1.6 trillion (€1.36 trillion). In 2025, growth is expected to remain below 1 percent and inflation is persistently high. This is a classic case of stagflation.

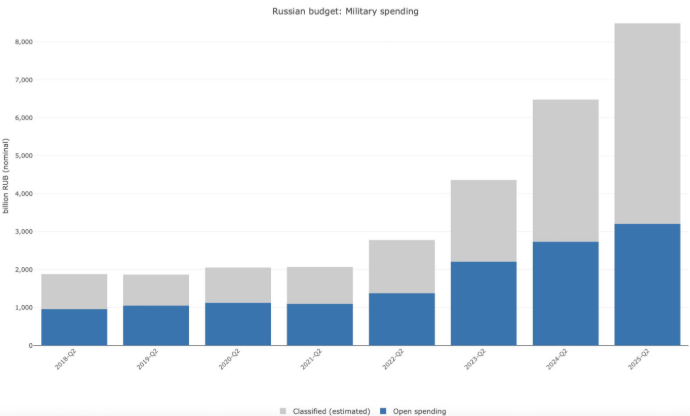

At the same time, the war imposes staggering costs on Moscow. According to The Moscow Times, at three times Ukraine’s rate, Russia’s daily outlay on mobilization, procurement, and logistics has reached a record level. Even by conservative calculations, this amounts to around $190 billion annually, which demonstrates the dramatic increase in the cost of the war. With the federal budget projected at about $410 billion (€347 billion), nearly one-quarter of state spending is absorbed by the war effort. Moreover, by mid-2025, 50.1 percent of budget revenues in January–March and 48.2 percent by the end of June had already been consumed by the war.

Moscow’s appetite for war continues to grow. Forbes Ukraine, citing Reuters, reports that between 2022 and 2024 Russia spent more than $250 billion (€212 billion) on its armed forces. Together with spending on ‘national security’, the security sector now absorbs more than 40 percent of the federal budget, pushing the projected deficit above $62 billion (€52.5 billion). Despite this, Russia continues to pour resources into its military. As I argue, only the economic exhaustion of Russia has the potential to lead to a ceasefire but, unfortunately, not to peace. This is why secondary sanctions matter.

Source: The Moscow Times. (2025, August 27). 47 billion rubles per day: Russia’s war spending hits a new record.

In sum, Moscow’s ability to finance its war machine depends heavily on fossil fuel revenues, while the fiscal burden of the war is eroding its long-term stability. These mounting vulnerabilities suggest that a tighter and better-enforced sanctions regime, especially secondary sanctions, could prove decisive in shifting the Kremlin’s cost–benefit calculation.

NATO unanimity: an impossible condition

By tying U.S. sanctions to NATO unanimity, Donald Trump has set the bar deliberately high. NATO, unlike the EU, includes members such as Turkey, Hungary, and Slovakia that maintain close ties with Moscow and remain among the biggest buyers of Russian oil. Expecting them to cut imports and fall into line on punitive measures is unrealistic. In practice, Trump’s condition amounts to deferring action indefinitely.

Trump is shifting the burden from Washington to European capitals

European Commission officials have signalled that Brussels will continue coordinating sanctions with international partners. But Trump’s framing shifts the burden from Washington to European capitals. For Moscow, this is a propaganda victory: it can point to NATO divisions, portray itself as an indispensable energy supplier, and use the breathing space to stabilise its war economy.

Tariffs on China: a risky distraction

The second condition set by Trump for U.S. sanctions demands that NATO members impose tariffs of 50–100 percent on China, only complicating matters further. Beijing remains the largest buyer of Russian oil, but it is also a central trading partner for the West. If action against Russia is made contingent on tariffs against China, this risks fracturing transatlantic unity at a time when Europe is already grappling with economic slowdown.

Tariffs are also a blunt instrument. As Nate Sibley notes for an article written for the Hudson Institute, punishing refiners and their financial backers in China, India, and Turkey through targeted secondary sanctions would be far more effective than sweeping tariffs, which could disrupt global supply chains. Trump’s proposal risks confusing objectives: the priority should be to weaken Moscow’s revenues, not to launch a trade war with Beijing.

How to make sanctions bite

The Hudson Institute offers a practical blueprint for turning sanctions from symbolic blows into strategic choke-points that could cripple Moscow’s war machine. First, it recommends neutralising the ‘shadow fleet’ of some 600 tankers that reflag and mask Russian crude shipments. Second, it urges targeting the refiners and the banks that underwrite them in China, India and Turkey. Third, it calls for much tougher export controls to stop Western components reaching Russian weapons factories through intermediaries. Fourth, it stresses the need for relentless pressure on the web of shell companies and front firms that facilitate evasion. Fifth, it argues for seizing frozen Russian sovereign assets, the hundreds of billions held in Western jurisdictions, and redirecting them to Ukraine. And sixth, it proposes squeezing overseas evasion hubs in places such as Georgia and parts of Africa, where Moscow’s networks buy influence and extract resources. Taken together and paired with steady military and budgetary support for Kyiv, these measures would not merely punish Russia; they would strike at the arteries of its war economy and force a costly recalculation in the Kremlin.

The Cost of concession

Trump’s shifting ultimatums are not rhetoric; they are strategic concessions. Each delay signals weakness to allies and opportunity to adversaries. By tying sanctions to NATO unanimity and broad tariffs on China, he shifts responsibility outward and slows action when pressure is most needed.

Russia exploits every pause. Cash keeps pouring in, its economy gains breathing space, and its propaganda points to Western division. The message is clear: energy exports remain safe, and time works in Moscow’s favour.

Russia exploits every pause

Ukraine, meanwhile, is left exposed. It is fiscally stretched, militarily under strain, and politically vulnerable as social contracts fray and resources are diverted to survival.

Sanctions cannot replace weapons, but they are essential to shrinking Moscow’s capacity to keep waging war. Combined with steady budgetary aid and military support, they can provide Ukraine not only with the means to resist, but also the ability to endure.

Comprehensive secondary sanctions on shipping insurance, financial services, and trading partners would strike at the core of Russia’s war economy. They could render its oil toxic, force deeper discounts, deter buyers, and raise transaction risks. Yet Trump’s conditions have deferred this prospect. Washington holds the cards but plays them conditionally, and every day of delay gives Moscow time to adapt, reroute, and sustain its war machine.

If the West seeks peace grounded in sovereignty and law, the moment is now to close the loopholes in Russia’s economic isolation, not to open new ones.

10 jaar RAAM: wij hebben uw hulp nodig

In 2026 bestaat RAAM 10 jaar. Het is geen vanzelfsprekendheid dat we blijven voortbestaan. Daarvoor hebben we uw hulp nodig. Met uw giften kunnen wij auteurs een bescheiden honorarium betalen, onderzoek doen en Kennisplatform RAAM overeind houden. Wij zijn een ANBI: uw gift is aftrekbaar van de belasting.

Oleksandra Moskalenko is the Willem F. Duisenberg Fellow at the Netherlands Institute for Advanced Study | Prof. (Political Economy), Dr.Sc. (Economics), Kyiv National Economic University named after Vadym Hetman | Visiting Professor, London School of Economics