Every day the war lasts we see new sanctions on Russia imposed by the West. How effective are they? Read the personal blog and newsletter of the Russian economist Sergey Aleksashenko if you want to stay informed about the tumultuous developments around the war in Ukraine and its financial impact. You can subscribe here.

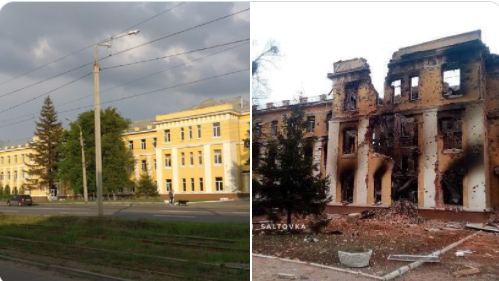

School in Ukrainian town Charkiv before and after Russian bombs (source: https://t.me/team_milov/1134)

School in Ukrainian town Charkiv before and after Russian bombs (source: https://t.me/team_milov/1134)

by Sergey Aleksashenko

After Russia started a war against Ukraine on February 24, Western countries imposed numerous sanctions against the aggressor country. Leaders of developed countries understand those imposed in recent days are unlikely to change the position of the Russian leader and will not stop the war. Still, they are confident that the sanctions imposed will substantially blow the Russian economy, undermining industrial potential and destabilizing financial markets. Is this true? My impression: they are much stronger than previously imposed on Russia, but I would not call them 'nuclear'. Too many loopholes.

The sanctions imposed are the strongest used by Western countries, after the sanctions against Iran in 2010 and North Korea in 2013. Russia is the largest economy and the largest country globally, by population, against which such strong sanctions have ever been imposed. All sanctions can be divided into three groups: Those aimed at isolation of the Russian financial system, the technological isolation of Russia, and the freedom of movement of Russian citizens and cargo around the world.

It will be difficult to pay

The first wave of financial sanctions has resulted, for Russia’s largest bank, Sberbank, 33% of the banking system’s assets, unable to make its payments and those of its customers denominated in dollars in four weeks. Its correspondent accounts with U.S. banks will be blocked. Four other banks, VTB, Otkritie, Novikombank, and Sovcombank, have been placed on the SDN List, which means their U.S. accounts and assets will be blocked entirely. This measure will also take effect in four weeks. In addition, the U.S. blocked 13 major Russian companies and banks from accessing its capital markets and banned U.S. investors from buying new issues of Russian government bonds in their initial public offerings and on the secondary market. In the second stage, the G7 countries decided to block the accounts and assets of the Central Bank of Russia (CBR) (we do not know from what date) and disconnect several Russian banks (names have not been made public) from the SWIFT system.

The Russian financial system is highly integrated into the global system. Russia is one of the largest raw materials suppliers to the world market. At the same time, the Russian economy is a significant importer of consumer goods, technology, and investment equipment. Russia’s exports account for 28.5% of GDP, with 85% being raw materials and primary products (hydrocarbons, metals, chemicals) and natural resources (agricultural products, timber, timber). Russia’s imports account for 18% of GDP; in 2021, 25% of the Russian food market and 50% of the non-food consumer goods market were imported products. For such an economy, international payments are critical; disconnecting the largest banks from making customer payments will disrupt goods flow, a consumer market deficit, and accelerate inflation.

The decision of Western countries not to limit payments related to payment for Russian energy exports (50% of exports) seems very rational: Europe guarantees the preservation of the stability of its energy system, and although currency proceeds from hydrocarbon exports will go to accounts in Russian banks, banks hit by sanctions will not be able to use these funds, because their correspondent accounts will be blocked.

The apparent weakness of the sanctions adopted to block international settlements for Russian banks and companies is that the scale of application of such sanctions by the European Union was significantly less than that of the United States, which leaves the possibility of virtually unlimited payments in euros.

Money does matter

The second most important mechanism of the impact of the sanctions on the Russian economy will be a ban on the access of Russian banks and companies to Western capital markets. If the statistics are believed, Russia’s foreign debt (sovereign and corporate debt, considering the debt of non-resident subsidiaries) is not too large. As of October 1, it was $490 billion (33% of GDP). However, from the point of view of its impact on the economy, it is not so much the amount of debt that matters, but the schedule for its repayment and the share of short-term debt.

According to the CBR, Russian banks and companies will have to repay at least $170 billion (10% of GDP) in the next 12 months. This is a hefty schedule, and many Russian borrowers counted on refinancing old debts. Now, this opportunity will be closed for many of them. Formally, the restriction on access to capital markets has been imposed on 25 banks and companies (including those for whom these sanctions were imposed in 2014). Still, I am sure that at least in the first 12 months after the war is over, no Russian company or bank will be able to access Western capital markets. This means that the Russian economy will have to channel substantial financial resources (similar to 2015)—about half of the future repayments (i.e., 5% of GDP)—to repay foreign debt. The only way to do this is to use domestic savings, undermining already weak economic growth.

Rely on China?

The obvious question is: Can China replace the West by providing its financial resources to Russia? The Russian leadership had such hopes in 2014-2016 after the annexation of Crimea, calling it a “pivot to the East.” However, those hopes were not destined to come true. While in Western markets, Russian borrowers talk to hundreds and thousands of investors, in China, there is only one such investor, the Communist Party. Despite numerous requests for loans from Putin, the government, and Russian companies, the amount was minimal and tied to Russia’s commitments to allow Chinese companies access to Russian production and exports. I do not see why China’s position would have to change today.

The strongest

Undoubtedly, the most powerful blow to the Russian financial system was the imposition of sanctions on the CBR (Central Bank of Russia), which plays a crucial role in functioning the domestic foreign exchange market. The CBR has enormous foreign exchange reserves ($630 billion, including $116 billion belonging to the Ministry of Finance of Russia). It traditionally acts as a “buyer/seller of last resort,” determining the level of the ruble exchange rate. The scale of currency interventions can be significant: In 15 months, after Russia annexed the Crimean Peninsula and attacked eastern Ukraine, from March 2014 to May 2015, the CBR spent $135 billion on currency interventions, more than 27% of its currency reserves at the time (including gold).

The freezing of the CBR’s assets and accounts in the G7 countries means that it is left with gold reserves ($115 billion, excluding the Finance Ministry) held in Russia and renminbi reserves (about $60 billion, of which $36 billion owned by the Finance Ministry). Both are useless from the point of view of maintaining stability in the domestic foreign exchange market.

The CBR loaned 2 trillion rubles (1.5% of GDP) to banks on Friday as part of its efforts to maintain stability in the financial system and promised to lend an additional 3 trillion rubles on Monday. Previously, banks used all the rubles they received to buy foreign currency in similar situations, and I expect the same this time.

If the sanctions against the CBR go into effect immediately, it will lead to a collapse of the currency market in Russia. By the end of Sunday, the selling rate of dollars in exchange offices of banks had risen by at least 45% compared to Friday. In such a situation, the most likely event is the freezing of the domestic currency market and the introduction of severe currency restrictions, including up to 100% mandatory sale of foreign exchange earnings by exporters and capital control measures. This would allow the CBR to organize currency trading between banks using mutual correspondent accounts and keep importers paying for their contracts. The price of functioning of such a system would be the actual abolition of supervisory standards—i.e., the loss of opportunities to control the real risks of the banking system.

Ruble devaluation will certainly affect consumer inflation, which may grow by 4%-5% with a 40%-50% ruble devaluation. In addition, disruptions in the payment system may lead to disruptions in the supply of imported goods to Russia, further accelerating inflation by reducing supply.

Long-lasting pressure

The second important block of sanctions is restrictions on exporting modern technology, technological equipment, and components to Russia. According to U.S. Department of the Treasury estimates, these sanctions cover about $50 billion worth of goods, or 35% of Russian imports of machinery, equipment, and technological goods. Export restrictions apply to military and dual-use products and products imported by Russian state-controlled companies; these sanctions are secondary—i.e., they apply to companies from any country if they use American equipment, technology, and patents.

These sanctions will seriously impact the technological level of the Russian economy: Russia has traditionally been an importer of advanced technology; imported components are used in all kinds of technologically complex products, from vacuum cleaners to nuclear-powered icebreakers. Many military products (weapons, communications equipment, optical devices) will be impossible to produce in Russia if sanctions remain.

But with few exceptions, the imposition of these sanctions will not lead to immediate effects: The practice of similar sanctions imposed in 2014-2016 showed that Russian defense sector companies had stocks of imported components that were sufficient for 12-18 months of production. Stopping investment projects in progress has a much more substantial impact on the economy’s future potential than on the current growth rate.

Iron Curtain 2.0

At the same time, for one sector of the Russian economy, aviation, the export sanctions will have a catastrophic impact. The EU sanctions have affected the supply of aircraft to Russia and the supply of components and the provision of aircraft maintenance services.

Analysis of the 20 largest Russian airlines (97% of passenger traffic) shows that 40% of the aircraft are made in the European Union (Airbus), and they carry 45% of the passengers. All of them fall under sanctions, and it should be expected that the ability to operate them will be reduced. The pressure of sanctions will be different for different companies. Still, it will be most vital for the two largest companies: Aeroflot operates 117 Airbus aircraft (185 aircraft in total in the fleet); S7 (the second largest) uses 66 Airbus (102 aircraft in full in the fleet).

Russia produces its narrow-body Superjet, which will not be able to replace Airbus: First, its capacity does not exceed 95 passengers, and its flight range is 4,800 km; second, this aircraft is produced in small numbers (41 in the past three years), and the restrictions imposed on the supply of components to the aviation industry will further slow down production; third, this aircraft has been in operation for ten years, but its “childhood diseases” have not yet been overcome, and its average flight time does not exceed 7 hours a day, which makes it impossible to achieve minimum efficiency.

A critical restriction that will substantially impact the current situation, but which is likely to be short-lived, is the closure by EU countries of their airspace to Russian aircraft, including business aviation. Flights to Europe are essential for Russian airlines because they are more profitable; they actively use transit flights from Asian countries to European countries. This restriction will affect the most affluent Russians who fly to Europe for business or leisure. Russian authorities have imposed similar bans on European airlines, which means a real Iron Curtain 2.0 for citizens.

This can be summarized as follows:

1) The imposed financial sanctions will be a severe blow to the Russian economy, destabilizing its economic and foreign exchange markets, disrupting import operations, and leading to ruble devaluation, rising inflation, and falling living standards of Russians.

2) The negative impact of financial sanctions will be offset by a solid current account balance, which relies on raw materials exports that are not threatened by anything. In addition, the unevenness of sanctions imposed by the European Union and the United States will allow the Russian authorities to avoid the most severe consequences.

3) The export restrictions imposed will undermine the capabilities of the Russian military and civilian industry, restrain the growth potential of the economy, and increase Russia’s technological backwardness.

4) The influence of financial sanctions will be most substantial in the first four-six months, after which it will weaken and may finally disappear in three-four years. In contrast, the influence of technological sanctions will be weak in the first months but will increase over time.

Behind the Iron Curtain is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. Subscribe here.